Are you financially divorced? 7 strategies to change the game

Authors: Daniel Brown and Ryan Bultitude

Reflecting on a common occurrence with new clients we meet, we have identified a new term: “financially divorced” i.e. to separate or disassociate from your financial situation, typically with an undesirable effect. These clients tend to come to us after trying to manage their own funds with little or no progress or having made uneducated decisions and following an inappropriate path for their financial situation.

Instead of disassociating yourself from your finances, take ownership and create influence over your financial outcome; with your retirement lifestyle being the end game.

“If you think financial advice is expensive, what about financial ignorance? It can cost you so much more in the end” Ryan Bultitude.

Here are some tips to support you to change your plans and take ownership of your financial tools:

1. Treat your finances like a business

Great businesses thrive when a complete and comprehensive knowledge of their numbers, expenditure and income exists.

Following their lead – analyse your expenses and income then review and reflect on how they are aligned to your financial goals.

There are three options of how you can spend money:

- you can spend money on items that have no value,

- you can invest money in defensive assets that will have a minimal return, but a return all the same, or

- you can invest in growth assets over the longer term, which can bring you to a position of wealth where you could potentially live off your earnings.

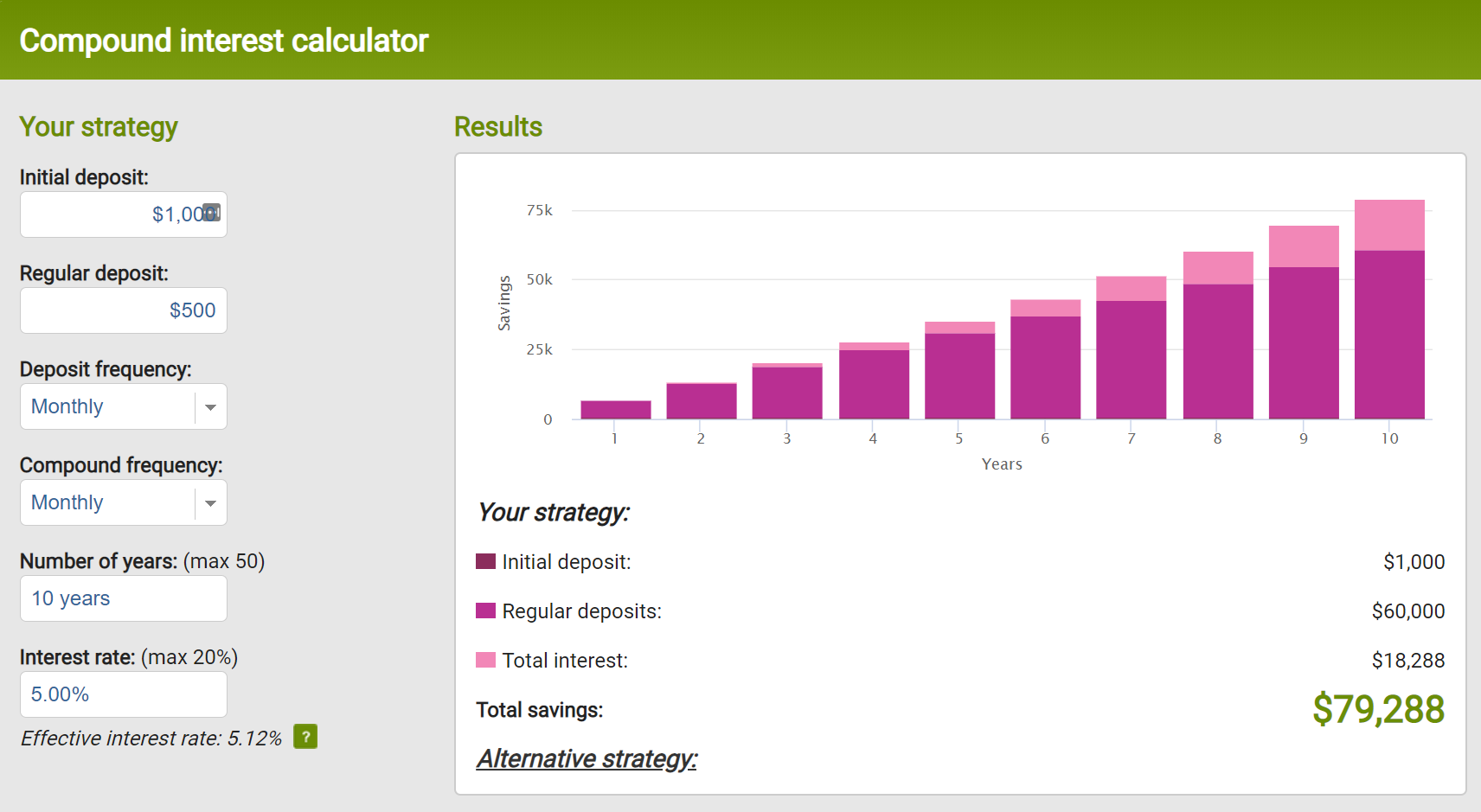

The attached image shows the value that compound interest can have on your savings. In this example, by commencing with an initial deposit of $1,000 and adding $500 per month to this, you can end up with nearly $80,000 in 10 years.

Source: https://www.moneysmart.gov.au/tools-and-resources/calculators-and-apps/compound-interest-calculator

Consider investing not only in financial assets but also in your financial education. Spending your time and money on a financial education will improve your overall financial literacy in turn guiding you to make more appropriate decisions.

2. Review the influences around you

Do the closest people around you encourage ownership, education, support, mentorship and provide insight on how they have achieved their goals?

Or

Do they simply put their head in the sand, not take responsibility and impart all of the excuses in the world, which in turn impacts your thinking?

Choose to spend your time with people that build up your confidence to make sound financial decisions and who support each other to attain financial independence on their journey.

3. Getting support – The benefit-to-cost ratio

What are the potential benefits and costs involved to have your Financial Adviser help achieve your goals? What are the costs and time involved to do it yourself? Can you do it yourself?

The adviser cost is irrelevant when you can capitalise on your adviser’s education, experience and access to opportunities to potentially grow your wealth substantially greater than those friends and associates who choose not to get financial advice.

Work with your adviser before something goes wrong – before you want to buy that next property but fall short, or before retirement approaches and you don’t have the assets required to live the lifestyle that you desired.

4. Understand your financial position

Ensure you understand the consequences of allocation options and the possible returns that one option has over another e.g. if you had a spare $50,000; would you deposit it:

- into a cash account returning 2% p.a.,

- in an offset account saving you 5% p.a. on interest accrual, or

- in an investment vehicle with the potential to earn you double figures?

Smart investment decisions are crucial. Do you have underperforming investment, such as property? Could your debt and wealth be earning increased revenue and capital gain returns? Are your financial investments not only earning the maximum returns, but also structured in the most tax effective manner?

Are you leveraging off good, tax-deductible debt for your investments, whereby you can claim interest for using the debt to create investment returns? Or are you highly leveraged on bad, non-tax-deductible debt that is a result of spending on material items that have no future value to you or your family?

5. Superannuation – likely to be your largest retirement asset

Understand and take control of your Superannuation!

Selecting appropriate investment options, understanding the fees, nominating beneficiaries and structuring appropriate insurance cover is a great starting point. Additionally, making extra contributions to build your super balance can also provide the ongoing benefit of compounding investment returns.

You can utilise your Superannuation as a vehicle to access more investment options, such as an active investment approach or the ability to invest in direct property.

The difference between a well-performing and underperforming fund can be the difference between retiring comfortably, or even in a position of wealth, versus living with very little weekly earnings.

6. Create a passive income source

Consider acquiring investment assets that produce additional income. Or choose the bolder step of establishing your own side hustle or online business.

Don’t work your whole life to stay alive, instead, work to setup a life where you don’t have to work.

Buy a lifestyle and buy time by putting measures in place now that will allow you to be rich in wealth and time.

7. Giving back – choose carefully

We all get asked for donations constantly and there is an unlimited amount of charity options available.

The best advice we have received about donations is: “Look after yourself first, then make donations you can afford”.

Understanding and taking responsibility for your expenses first provides the opportunity to really get behind your charities of choice later. Ensuring your financial position is secure can allow you to make meaningful financial donations as well as giving the gift of your time.

“Rich people believe ‘I create my life.’ Poor people believe ‘Life happens to me.’” T. Harv Eker

Register now for our free 30-minute goal setting coaching session, or better still, act now and book a financial planning meeting with one of our goal setting specialists.

DJIB Investments Pty Ltd T/A Central Coast Financial Planning Group is a Corporate Authorised Representative of RI Advice Group Pty Ltd, ABN 23 001 774 125 AFSL 238429. This editorial does not consider your personal circumstances and is general advice only. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide. If you no longer want to receive this information, please contact our office to opt out. The views expressed in this publication are solely those of the author; they are not reflective or indicative of Licensee’s position and are not to be attributed to the Licensee. They cannot be reproduced in any form without the express written consent of the author.